Jobs data released by the Bureau of Labor Statistics at the start of May showed that, despite challenges across several sectors of the economy, the U.S. labor market continued to show resilience: 253,000 new jobs were added and the unemployment rate remained relatively stable below 3.5%. Plus, some economists noted that, even with such low unemployment numbers and a strong employment market, the gig workforce continued to grow.

Whether it’s freelance work in addition to a “day job,” full-time freelance for maximum flexibility, or temporary freelance work between traditional employment opportunities, gig workers in a wide variety of occupations are estimated to represent as much as 15% of the workforce.

Of course, no matter the occupation, making the most out of the possibilities of gig work can depend greatly on location. As such, we set out to identify the U.S. metros with the best gig economy potential. To that end, we compared more than 70 of the most populous metropolitan areas in the U.S. and scored them across several indicators, which could add up to a maximum total score of 100 points (see the methodology section for details).

Read on for our findings on the top 20 U.S. metros for gig workers, as well as highlights for each of the four major regions in the U.S. Additionally, following our metro area ranking highlights are insightful contributions from gig economy work experts who share their takes on what drives success in the gig economy and what transformational potential it harbors.

Top 20 U.S. Metros for Gig Work

The Miami metropolitan area earned the highest overall score (65 points) and took the #1 spot in our ranking. With a little more than 17,860 non-employer establishments per 100,000 residents, Miami stood out for the highest ratio of self-employed residents out of all of the metros we compared for this ranking. Notably, the metro also boasted one of the 10 highest rates of growth for non-employer establishments: With an increase of 23.2% throughout five years, Miami was roughly on par with San Antonio, Texas, as well as very close behind Jacksonville, Fla. (23.3%).

Freelancers in need of flexible workspace here will find that the South Florida metro boasts the third-highest coworking space density — an estimated 3.9 coworking spaces per 100,000 residents. What’s more, Miami coworking space also ranked among the top 10 most affordable on our list with a median price of $99 per person per month.

The second-best U.S. metro for gig work was Nashville, Tenn., which earned a total score of nearly 65 points. The annual median earnings for self-employed residents operating unincorporated businesses here was roughly $34,600 — fifth-highest among the metros we compared and not far behind Boston; Austin, Texas; New Haven, Conn.; and San Francisco. Nashville also scored among the top 10 for density of non-employer establishments: Its ratio of 10,086 businesses per 100,000 residents scored ninth-best, ahead of Houston and behind the New York metro area. Meanwhile, the density of coworking spaces in Nashville (2.9 per 100,000 residents) scored roughly on par with Dallas and Indianapolis, as well as closely behind San Jose, Calif. (3.1/100,000).

At the same time, Austin, Texas, was the third-best metro for the gig economy, with a little more than 62 points out of 100. Specifically, the hip Texas metro was home to the seventh-highest density of non-employer establishments (10,168 per 100,000 residents), scoring closely behind New Orleans. Moreover, non-employer numbers here increased 24.4% throughout five years, which represented the fourth-largest such growth among the metros we compared. However, Austin ranked even better in terms of earnings: Self-employed residents operating unincorporated businesses in the Austin-Round Rock metropolitan statistical area (MSA) had annual median earnings of $34,898. Notably, that was the third-largest in our ranking, behind only New Haven, Conn., and San Francisco. Accordingly, freelance professionals here also have a relatively abundant choice of flexible workspace: Austin coworking space had the fifth-highest density in our ranking (3.6 coworking spaces per 100,000 residents).

Next, the Denver metropolitan area continued to rank among the best places for entrepreneurial professionals. With a total score of almost 62 points, Denver ranked as the fourth-best U.S. metro for gig work. In particular, its strongest-performing indicator was flexible workspace density. In fact, Denver’s coworking space ratio of 4.4 spaces per 100,000 residents was the highest among the 71 metros we compared, followed by Washington, D.C. and Miami. Here, the number of non-employer establishments increased by nearly 17% in five years. And, according to the most recent Census Nonemployer Statistics (NES) data, the Mile High City also reached a density of roughly 9,880 per 100,000 residents (12th-largest in our ranking). Furthermore, the annual median earnings of self-employed Denver metro residents operating unincorporated businesses ranked 11th-highest, which placed Denver ahead of both Baltimore and Washington, D.C.

The fifth-best score went to the Orlando, Fla., metropolitan area. The MSA rounded out the top five with a little more than 60 points in total, ahead of in-state neighbors Jacksonville and Tampa. Namely, the central Florida MSA showed the second-largest increase in the number of non-employer establishments — 29.7% in five years — ahead of Houston and second only to the Las Vegas MSA. On the heels of that growth, Orlando was also home to the third-highest non-employer establishment density (10,925 per 100,000 residents) among the metros in our ranking, ahead of Los Angeles and behind only Atlanta and Miami.

Florida Entries Outperform Most Other Southern U.S. Metros in the Gig Work Ranking

Of the 71 metros included in our current ranking, 28 are located in the Southern U.S., making it the largest regional group in the mix. Additionally, all 10 of the top-scoring Southern U.S. metros highlighted below also ranked among the best 20 metros nationally.

For instance, the Florida-Tennessee-Texas trio of Miami, Nashville, and Austin MSAs also claimed the top three spots in the top 10 Southern U.S. regional ranking. They were followed by strong Florida representation: Orlando came in as the fourth-best metro for gig work among the Southern U.S. metros we compared, besting Jacksonville in fifth place and Tampa in sixth.

That said, Jacksonville’s strongest-performing indicator was income growth: The annual median earnings of self-employed metro residents operating unincorporated businesses here increased 32.3% in five years — the highest such increase among the top 10 metros in the region. And, with a 23.3% increase in the number of non-employer establishments in five years, Jacksonville also scored fifth-best in the region for non-employer business growth.

For that metric, Jacksonville came in close behind Tampa, where the number of non-employer businesses grew 24.4% in five years. Here, gig-oriented professionals in need of flexible offices benefit from some of the most affordable options in the region, as both Jacksonville and Tampa coworking space was estimated at a median price of $93 per person per month.

In the West, Las Vegas & Los Angeles Earn Top Scores for Non-Employer Business Numbers

The second-largest regional group in the mix was represented by Western U.S. metros, which accounted for 18 of the 71 metros we compared for this ranking. It’s worth noting that six of the regional selections included here also ranked among the top 20 U.S. metros for gig workers — Denver; Las Vegas; Phoenix; Salt Lake City; Provo, Utah; and San Jose, Calif.

First, Las Vegas boasted the highest rate of growth for non-employer establishments in the region with an increase of 31.3% throughout five years. This marked a larger rate of growth than was recorded in similarly sized metro areas, such as Denver.

Even so, the largest non-employer business sector in the Western U.S. region was in Los Angeles, which was home to 10,888 non-employer establishments — ahead of Denver and San Francisco. Moreover, Los Angeles was also home to one of the most abundant coworking space scenes in the Western U.S.: There were 3.4 coworking spaces per 100,000 metro residents here, behind only San Diego and Denver.

In terms of coworking space cost, the metros offering the most affordable options in the region were San Jose, Calif.; Phoenix; Las Vegas; and Provo, Utah, where the median price for open coworking space was $93 per person per month.

Indianapolis & Chicago Rank Best in Midwest for Non-Employer Business & Coworking Space

Not to be outdone, the Midwestern U.S. region was home to 14 of the 71 cities analyzed for this gig economy work ranking. In particular, Indianapolis — which came in 14th among the top 20 metros nationally — earned the top score on a regional level: The MSA’s best-scoring indicators were earnings growth and coworking space density. Specifically, the annual median earnings of self-employed metro residents operating unincorporated businesses here increased 28.4% in five years, which placed Indianapolis first in the region for earnings growth. Likewise, with a ratio of 2.9 coworking spaces per 100,000 metro residents, Indianapolis was also home to the highest coworking space density in the Midwestern U.S. region, followed by Madison and Chicago.

Next was Chicago, which placed outside the top 20 best metros nationwide, but nevertheless earned top scores on a regional level for non-employer business representation and coworking space affordability. More precisely, Chicago was home to the highest density of non-employer businesses — an indicator for which it ranked ahead of Detroit and Columbus. The Illinois MSA also scored best in the region for flexible office space cost: The median price for open coworking space memberships in Chicago was $95 per person per month.

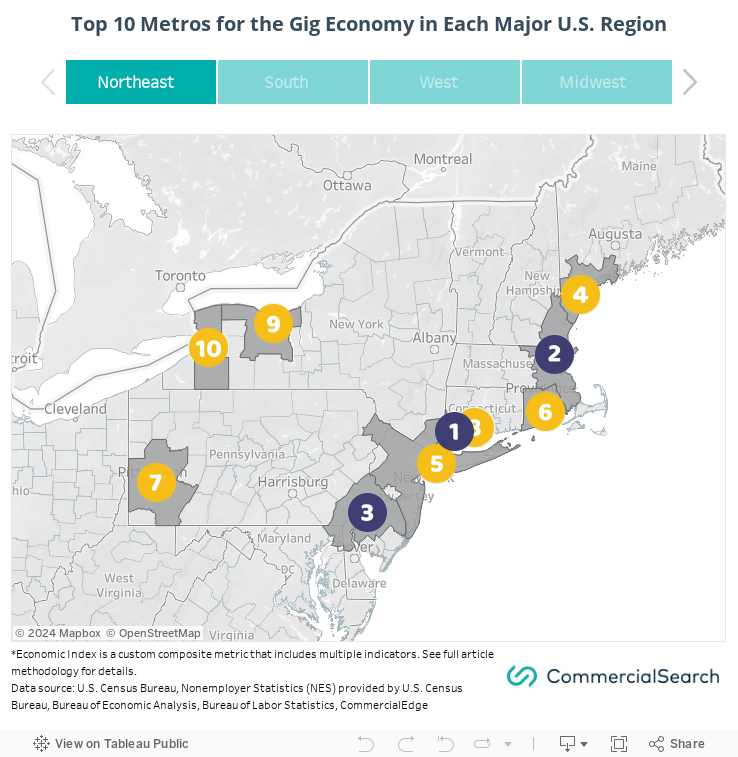

In the Northeast, New York Trails Bridgeport for Non-Employer Business Density

The Bridgeport, Conn., metropolitan statistical area was the only Northeastern U.S. metro to rank among the top 20 in the country. With a total score of almost 54 points, Bridgeport came in 12th nationally, but took the top spot on a regional level. Its best-scoring indicators were non-employer business representation and coworking space affordability.

In this case, Bridgeport’s ratio of 10,479 non-employer establishments per 100,000 metro residents was the highest non-employer business density among the Northeastern U.S. metros we compared. The neighboring (and more populous) New York metropolitan area followed in second place with a ratio of 10,165 per 100,000 residents.

Moreover, Bridgeport’s coworking scene ranked among the best for both of the indicators we analyzed: With 2.7 coworking spaces per 100,000 metro residents, Bridgeport tied Boston for the highest coworking space density in the region. And, at a median price of $93 per person per month for an open coworking space membership, Bridgeport also tied Philadelphia for most affordable coworking space among Northeastern U.S. metros.

Although the gig work model still has room to improve in terms of economic relationships and gig-friendly economic policies, its greatest advantage keeps it growing: It makes work highly adaptable to the needs of the moment and addresses the increasing demand for flexibility that stems from our increasingly complex lives.

Furthermore, in the gig work economy, companies have access to freelance, flexible talent, while professionals lending themselves to gig work (whether full-time or in addition to traditional employment) have access to more diverse and flexible professional opportunities. Yet, there’s more to the gig economy than its basic mechanisms. To that end, we asked a few experts to comment on what drives the gig economy, how it contributes to the larger picture, and what transformational potential it carries for our future. Read their insights in the interviews below.

Kathy Kristof

is an award-winning financial journalist and author who has contributed to publications including The Los Angeles Times, CBS News, Inc., Kiplinger, and Forbes. She’s also authored three books, including the widely appreciated “Investing 101,” and is now the gig economy editor of SideHusl.com — a platform that seeks to create an open, fair, and transparent marketplace for freelancers.

is an award-winning financial journalist and author who has contributed to publications including The Los Angeles Times, CBS News, Inc., Kiplinger, and Forbes. She’s also authored three books, including the widely appreciated “Investing 101,” and is now the gig economy editor of SideHusl.com — a platform that seeks to create an open, fair, and transparent marketplace for freelancers.

Q: Would you say that growth of the gig economy is more a consequence of a highly dynamic employment landscape, or of workers needing to keep up with a galloping cost of living?

K. Kristof: "In the past, the side hustle market was growing through new opportunity. This year, however, the growth engine was hit with the rocket fuel of inflation to really take off. Even though the latest jobs report indicates that jobs are definitely coming back, paychecks are not rising nearly as fast as inflation. As a result, people are increasingly turning to side hustles to make extra money."

Q: U.S. history is a rich collection of industry transformation driving fast progress. Is there something about gig work that might harbor that kind of transformational potential for the future?

K. Kristof: "Yes. The flexibility for both workers and companies is astounding and desperately needed, which makes me believe that this industry is just getting started. I’m increasingly seeing ‘staffing’ companies emerge that solve the benefits problem for workers, while solving the inconsistent demand problem for companies. This creates the best of all possible worlds — where workers can decide when and where they want to work, without having to give up access to health insurance and other earned employee benefits. Meanwhile, companies have a ready workforce that can span geographies, making it easier for them to expand — and contract, when necessary — without the sometimes-crippling cost of adding/letting go of permanent workers."

Q: What is an aspect of gig work that can be beneficial both for gig workers and for gig employers?

K. Kristof: "Flexibility ... see above. It’s in the win-wins that you see the world transform"

Q: The need to adapt fast and well during the past few years has contributed to an increased need for flexibility — both across the workforce and for some businesses, which seems to send ripples through real estate. To what degree might we expect the gig economy to transform office leasing in the coming years?

K. Kristof: "Funny you should ask. I used to own real estate investment trusts, which own commercial properties. A year into the pandemic, I sold them. Why? People learned that they could successfully work from home and better balance work/life responsibilities. That’s a genie that’s very difficult to stuff back into a bottle. To be sure, some people have gone back to working in offices ... but many have opted to work from home. I think that’s going to have a compelling impact on the commercial real estate industry for years to come."

Marianne Olsson

Marianne Olsson is a gig economy and consulting expert and strategic advisor with 25 years of marketing and business development experience in international environments. She has authored more than 10 books, the latest of which include “Consulting in the Gig Economy” and “Working in the Gig Economy,” a series that describes the new job market and aims to help readers figure out how they can adapt in order to be chosen for assignments and gig work, as well as where to find it.

Marianne Olsson is a gig economy and consulting expert and strategic advisor with 25 years of marketing and business development experience in international environments. She has authored more than 10 books, the latest of which include “Consulting in the Gig Economy” and “Working in the Gig Economy,” a series that describes the new job market and aims to help readers figure out how they can adapt in order to be chosen for assignments and gig work, as well as where to find it.

Q: Would you say that growth of gig work is more a consequence of a highly dynamic employment landscape, or of workers needing to keep up with a galloping cost of living?

M. Olsson: "It’s a combination of driving forces. And, looking at the external environment and the digital landscape, there are so many opportunities for all stakeholders — both the employers or purchasers and the gig workers or workforce in general."

Q: U.S. history is a rich collection of industry transformation driving fast progress. Is there something about the gig economy that might harbor that kind of transformational potential for the future?

M. Olsson: "I believe that we are already there. The companies that grasp the ever-changing and fast-developing market (driven by digital opportunities) will outperform their competition, by far."

Q: What is an aspect of gig work that can be beneficial both for gig workers and for gig employers?

M. Olsson: "There are benefits for both in terms of flexibility. It can be smart for scaling up a company with temp resources (freelancers or gig workers, depending on the job description). The gig workers can choose to work hours that match their preferred lifestyle or schedule, for example. Also earning during peaks, where there is a lot of work in a smaller window of available gigs."

Q: The need to adapt fast and well during the past few years has contributed to an increased need for flexibility — both across the workforce and for some businesses, which seems to send ripples through real estate. To what degree might we expect the gig economy to transform office leasing in the coming years?

M. Olsson: "The real estate industry and office leasing especially are in the middle of a major transition, which is really interesting since it has been a conservative industry that now needs a higher pace of change and adaptation to new market conditions. The concept of traditional office space will always be needed and the challenge and opportunity is to adapt the service offering according to new needs among companies and gig workers alike."

Gali Arnon

has served as chief marketing officer since 2017 at Fiverr, a leading global online marketplace for digital freelance services that connects businesses with a global network of remote freelancers.

has served as chief marketing officer since 2017 at Fiverr, a leading global online marketplace for digital freelance services that connects businesses with a global network of remote freelancers.

Q: Would you say that growth of the gig economy is more a consequence of a highly dynamic employment landscape, or of workers needing to keep up with a galloping cost of living?

G. Arnon: "If I had to pick between the two, I’d say the rise of the freelance economy is more a consequence of a highly dynamic and accessible employment landscape. I say accessible because we are seeing more workers — the world over — using freelance platforms (like Fiverr.com) to connect with businesses, find exciting work opportunities, and create lasting relationships.

"According to Fiverr’s recent Freelance Economic Impact Report released last week, U.S. freelancers are estimated to have earned $286 billion in revenue in 2022, up 9.2% from 2021. What’s driving the numbers? There are many reasons more people are choosing to freelance. They want flexibility, not to be tied down to a 9 to 5. They want control over their workload, to be their own boss. It’s also about security. Freelancing allows a person to diversify their income. The report found [that] over 80% of independent workers strongly or somewhat agree that having multiple sources of income provides a greater level of security than relying on a single employer."

Q: U.S. history is a rich collection of industry transformation driving fast progress. Is there something about the gig economy that might harbor that kind of transformational potential for the future?

G. Arnon: “Absolutely. Freelancers are often a bellwether for larger industry trends. They know business needs before the regular employee because they are tapped to fill those holes first. Furthermore, because freelancers on Fiverr are in different countries, they are bringing fresh, inventive ideas across borders. This democratization of talent certainly can harbor transformation potential for industries the world over.”

Q: What is an aspect of gig work that can be beneficial both for gig workers and for gig employers?

G. Arnon: "I can talk to the freelance economy, where workers have specific skills that businesses need and that is flexibility and agility. At Fiverr, we like to say we’re fostering an environment for ‘organic enterprises.’ What we mean by that is, as businesses expand in good times and contract in leaner times, our platform is there to assist.

"When onboarding freelancers, businesses need hiring and talent management assistance to enable freelance workers to work seamlessly alongside full-time staff. To attract top talent means understanding how that talent wants to work — not the other way around.

"Freelancers also want flexibility. This is why they have chosen to pursue this lifestyle. A platform like Fiverr allows them to show they are available and spend their time focusing on doing great work. They don’t want to be applying for new jobs. Fiverr does the heavy lifting of marketing freelancers’ services and matching them with the right hiring managers"

Q: The need to adapt fast and well during the past few years has contributed to an increased need for flexibility — both across the workforce and for some businesses, which seems to send ripples through real estate. To what degree might we expect the gig economy to transform office leasing in the coming years?

G. Arnon: "We at Fiverr are firm believers that great work can be done digitally. Our platform is global, and we have hundreds of thousands of freelancers working with millions of businesses across borders. Freelancers like to work from where they’re comfortable, whether that’s at home, a coffee shop or an office."

Pavel Shynkarenko

is the co-founder and CEO of Solar Staff, an international fintech company that enables businesses to connect with freelancers from more than 190 countries. Its mission is to bridge companies from developed economies with freelancers from developing regions, thereby transforming international freelance into local, barrier-free work opportunities.

is the co-founder and CEO of Solar Staff, an international fintech company that enables businesses to connect with freelancers from more than 190 countries. Its mission is to bridge companies from developed economies with freelancers from developing regions, thereby transforming international freelance into local, barrier-free work opportunities.

Q: Would you say that growth of the gig economy is more a consequence of a highly dynamic employment landscape, or of workers needing to keep up with a galloping cost of living?

P. Shynkarenko: "I think growth of the gig economy is generally related to the acceleration of the pace of life; the pace of doing business; inflation; and many other social and economic processes, and the gig economy is just a response to this acceleration. As consumers, we want everything right now. As businesses, we want a growth rate that resembles a hockey stick graph. As employees, we want our income to grow at an accelerating pace, and this is the mechanism that constantly accelerates itself. In this mechanism, the gig economy is a tool that allows us to keep up with the pace of business growth, as well as the pace of desirable income growth for gig workers, so that is beneficial for both parties."

Q: U.S. history is a rich collection of industry transformation driving fast progress. Is there something about the gig economy that might harbor that kind of transformational potential for the future?

P. Shynkarenko: "I think that there may be a whole series of significant changes brewing in the gig economy, which may fuel it and cause business transformations. The first is related to government regulation, which will lead to the establishment of equal conditions; a reduction in investment risks; and consequently, growth in this sector. To understand how significant it is, one can recall Uber and the dozens of investor rejections at the early stages precisely for regulatory reasons.

"Furthermore, the development of AI is capable of enhancing the abilities of gig workers, such as knowledge workers, and it may become a kind of ‘exoskeleton’ for them, significantly increasing their efficiency and putting them in competition not only with small companies, but even with medium and large businesses. That means many processes will be easier and faster and will drive further economic transformations.

"A simple example: A company needs to launch a product quickly and try to enter the market. The search for an average, full-time employee — as well as the search for a contractor company — takes 30 days, while the search for a freelancer can take up to three days, so the product will enter the market much quicker."

Q: What is an aspect of gig work that can be beneficial both for gig workers and for gig employers?

P. Shynkarenko: "It is flexibility. It gives the employer the flexibility to use freelance services when needed and for the period of time needed, and it also gives them the ability to use expert experience for one-time tasks. For example, a business needs to launch outdoor advertising in Mexico. The marketing team has never done so. Hiring a freelancer with that expertise will help solve the problem.

"The same flexibility is highly valued by freelancers. According to a recent talent research, flexibility took second place in determining (after the compensation) whether the workers are satisfied with their work or not: [A] stunning 93% of knowledge workers want a flexible schedule and 76% want flexibility in where they work, and that means working from anywhere, not from a classic office."

Q: The need to adapt fast and well during the past few years has contributed to an increased need for flexibility — both across the workforce and for some businesses, which seems to send ripples through real estate. To what degree might we expect the gig economy to transform office leasing in the coming years?

P. Shynkarenko: "I don’t think that there is a linear relationship between gig economy development and office leasing. There will be changes but, in my opinion, the offices will change more due to the overall shift in human labor or due to the redistribution of roles within and outside the team. We will see more office spaces that are designed not only for those who are constantly present in them, but also for those who periodically come in to communicate more effectively with each other. The high percentage of knowledge workers wanting flexibility in when and where they work confirms this trend."

Methodology

For this analysis, we looked at U.S. metropolitan statistical areas (MSA) with populations of 500,000 or more. Population totals considered for city selection were according to U.S. Census Bureau estimates for 2021. This criterion was not factored into the scoring system.

We sourced data from the U.S. Census Bureau (Census), the U.S. Bureau of Labor Statistics (BLS), the U.S. Bureau of Economic Analysis (BEA), and CommercialEdge Research. We employed the most recent data available from each source. Data scored for each metric was at MSA level. To each MSA, we assigned composite scores based on seven metrics (indicators).

For each metric, the number of maximum points was evenly distributed between the lowest and highest metric values within the group. On this scale, a score was calculated for each MSA based on its metric values. Scores for the top 20 MSAs were the result of comparison across the entire set of 71 metropolitan areas considered for this ranking. Conversely, MSA scores in the breakdown by U.S. region were the result of comparison across each respective regional subset.

For most indicators, the number of points awarded was directly proportional to the metric values. However, points were inversely awarded for: coworking space median prices, unemployment rate, and regional price parity. Each MSA’s overall score was then calculated by adding the scores for each metric. The indicators (metrics) on which we based the composite scores are explained below.

Non-Employers Per 100,000 Residents Ratio

The Census Nonemployer Statistics report published in 2022 considered that most non-employers were self-employed individuals who operated unincorporated businesses (also known as sole proprietorships), which may or may not be their principal source of income. For this ratio, we considered the number of non-employer establishments per 100,000 residents in each MSA. The maximum weight for this metric was 15 points.

Non-Employer Growth

To gauge the evolution of non-employer businesses in each metro, we compared the most recently available employment data with employment data from five years prior (2019 to 2015). The value scored represented change (either positive or negative) in the number of non-employer establishments for each MSA. The maximum weight for this metric was 15 points.

Median Earnings

Values scored for median earnings represented the annual median income for self-employed individuals aged 16 and up who were operating unincorporated businesses, as reflected in the most recent Census data. The maximum weight for this metric was 15 points.

Median Earnings Growth

To gauge the change in median earnings in five years, we compared 2017 income data with 2021 income data. The value scored for each metro represented the percentage change (either positive or negative) of median annual earnings of self-employed individuals aged 16 and up who were operating unincorporated businesses. The maximum weight for this metric was 15 points.

Economic Index

This indicator totaled a maximum of 15 points and included three metrics, which were each awarded a maximum of five points: the inflation-adjusted median household income for 12 months, as available in the most recent Census data; the regional price parity for each metro area, as reported by the latest BEA data available; and the unemployment rate for each location, as recorded in the most recently available BLS data.

Coworking Space Per 100,000 Residents Ratio

This indicator expressed the ratio of coworking spaces per 100,000 metropolitan area residents, as estimated based on CommercialEdge coworking space research data. The maximum weight for this metric was 15 points.

Coworking Space Cost

We also turned to CommercialEdge coworking market research data for estimates on coworking space cost in each of the metropolitan areas included in our study. This indicator was calculated for MSAs where there were at least five coworking spaces listed and expressed the median price for open coworking space per person per month. The maximum weight for this metric was 10 points.

For the regional breakdown of our analysis, we followed the U.S. Census region divisions:

- Western U.S.: Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington, and Wyoming.

- Midwestern U.S.: Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, and Wisconsin.

- Southern U.S.: Alabama, Arkansas, Delaware, Florida, Georgia, Kentucky, Louisiana, Maryland, Mississippi, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, Virginia, and West Virginia, as well as Washington, D.C.

- Northeast U.S.: Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, and Vermont.

Disclaimer

While every effort was made to ensure the timeliness and accuracy of the information presented herein, the information is provided “as is” and neither CommercialSearch nor CommercialEdge can guarantee that the information provided is complete. This report is published for general informational purposes only. It does not constitute and should not be relied upon as a basis for any investment decision. The information presented is subject to change without notice and may or may not apply depending on the circumstances. Always contact a qualified investment consultant if you need advice regarding buying, selling or otherwise transacting in any investment.